File & Defend Cheque Bounce Case in India – A Complete Guide

Cheque bounce case in India is buzzing, a dynamic business environment, and cheques continue to be a cornerstone of financial transactions. However, the cheque dishonour, commonly known as a “cheque bounce,” is a serious issue that can disrupt cash flow and lead to significant legal disputes. Understanding your rights and the correct legal procedure is paramount, whether you are the one who received the bounced cheque or the one who issued it.

At Kapil Dixit LLP, we provide expert legal guidance through the intricate landscape of cheque bounce litigation. This comprehensive guide leverages our deep expertise to walk you through the entire process under Section 138 of the Negotiable Instruments Act, 1881 (NI Act), covering everything from filing a complaint to mounting a robust defense.

Understanding the Legal Foundation: Section 138 of the NI Act

Section 138 of the NI Act criminalizes the act of issuing a cheque that is subsequently dishonoured. The provision was enacted to enhance the credibility of cheques and enforce financial accountability.

For a cheque bounce to become a criminal offence under Section 138, the following conditions must be met:

|

Condition |

Explanation |

|---|---|

|

1. Legally Enforceable Debt |

The cheque must have been issued to discharge a legally valid and recoverable debt or liability. Cheques issued as gifts, donations, or as a security deposit where the primary obligation has not yet arisen may not qualify. |

|

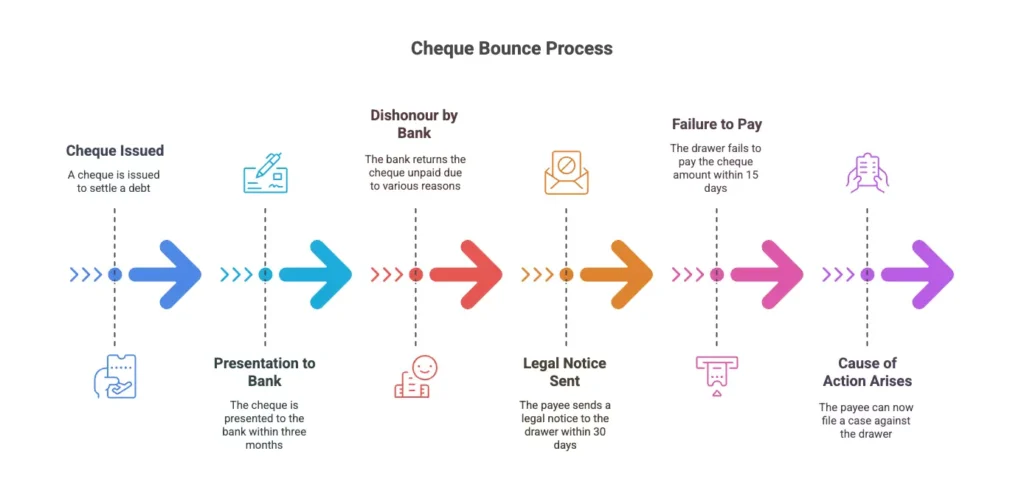

2. Presentation Within Validity |

The cheque must be presented to the bank within three months of its date of issue. |

|

3. Dishonour by the Bank |

The bank must return the cheque unpaid. Common reasons include “insufficient funds,” “account closed,” “payment stopped by drawer,” or “exceeds arrangement.” |

|

4. Issuance of a Legal Notice |

The payee (the person who received the cheque) must send a written demand notice to the drawer within 30 days of receiving the cheque return memo from the bank. |

|

5. Failure to Pay |

The drawer must fail to pay the full cheque amount within 15 days of receiving the legal notice. The cause of action to file a case arises only after this 15-day period expires. |

The Supreme Court, in cases like K. Bhaskaran v. Sankaran Vaidhyan Balan, has affirmed that all five of these components must be fulfilled to constitute an offence.

How to File a Cheque Bounce Case in India: A Step-by-Step Guide for the Complainant

If you have received a bounced cheque, acting swiftly and systematically is key to recovering your money. Here is the plan of action:

Step 1: Send a Formal Demand Notice

Within 30 days of the cheque dishonour, you must send a legal notice to the drawer. This notice should:

- Clearly state the details of the cheque dishonour (number, date, amount).

- Mention that the cheque was issued for a legally enforceable debt.

- Demand payment of the full cheque amount within 15 days.

- Warn of legal action under Section 138 of the NI Act if payment is not made.

Tip: Always send the notice via Registered Post with Acknowledgment Due (RPAD) to have valid proof of service.

Step 2: File a Criminal Complaint

If the drawer fails to pay within the 15-day notice period, you can file a criminal complaint with a Judicial Magistrate of the First Class. This complaint must be filed within 30 days from the expiry of the 15-day notice period.

Step 3: Jurisdiction of the Court

Thanks to the 2015 amendment to the NI Act, the jurisdiction for filing the case lies with the court where the payee’s bank branch is located. This was clarified by the Supreme Court in Bridgestone India Pvt. Ltd. v. Inderpal Singh and offers significant convenience to the complainant.

Step 4: Court Proceedings and Trial for Cheque Bounce Case in India

Once the complaint is filed, the court will examine the documents and the complainant’s statement. If a prima facie case is established, a summons will be issued to the accused.

Most cheque bounce cases in India are conducted as summary trials for a speedier resolution.

Documents Needed to File a Cheque Bounce Case:

- The original dishonoured cheque.

- The cheque return memo from the bank.

- A copy of the legal notice was sent to the drawer.

- Proof of service of the notice (e.g., postal receipt, tracking report).

- An affidavit by the complainant verifying the facts.

How to Defend a Cheque Bounce Case in India: Legal Strategies for the Accused

If you are facing a Section 138 complaint, you have the right to a fair defense. The burden of proof is on the complainant, and the accused can rebut the presumptions of the law.

Key Legal Defenses:

- No Legally Enforceable Debt: This is the most common defense. You can argue that the cheque was not issued for a valid debt. For example, it was given as a security deposit, for a time-barred debt, or as a gift.

- Misuse of a Security Cheque: If you can prove that the cheque was issued as security and the primary condition for its encashment was not met, the case may be dismissed.

- Procedural Lapses by the Complainant: Any failure by the complainant to adhere to the strict timelines (e.g., sending the notice after 30 days or filing the complaint after the limitation period) can be a fatal flaw in their case.

- Material Alteration of Cheque: If the complainant has made unauthorized changes to the cheque, it becomes void.

- Cheque Was Lost or Stolen: This defense is viable only if you have promptly filed an FIR and informed your bank to stop payment.

In K. Prakashan v. P.K. Surenderan, the Supreme Court held that the complainant must prove the existence of a legally enforceable debt for a conviction to stand. A mere issuance of a cheque is not enough.

Strategic Action for the Accused:

- Reply to the Legal Notice: Immediately send a detailed reply to the notice, stating your defense clearly.

- Gather Evidence: Collect all relevant documents, such as bank statements, loan closure certificates, emails, or WhatsApp chats that support your defense.

- Consider Quashing: If the complaint is malicious or legally flawed, you can approach the High Court under Section 482 of the CrPC to have the proceedings quashed.

Penalties, Settlement, and Recent Developments

Punishment on Conviction:

If found guilty, the drawer can face:

- Imprisonment for a term of up to two years.

- A fine of up to twice the amount of the cheque.

- Or both.

Compounding of Offence (Settlement):

Section 147 of the NI Act makes the offence compoundable, meaning the parties can settle the dispute at any stage. The Supreme Court encourages this and has even laid down guidelines for imposing graded costs to promote early settlement. Platforms like Lok Adalats and mediation are highly effective for resolving these matters amicably.

Recent Legal Reforms:

- Interim Compensation (Section 143A): The court now has the power to direct the drawer to pay up to 20% of the cheque amount as interim compensation to the complainant during the trial.

- Deposit During Appeal (Section 148): If convicted, the drawer may be required to deposit a minimum of 20% of the fine or compensation amount when filing an appeal.

Frequently Asked Questions (FAQ’s)

Q1. What is a cheque bounce case in India and when does it become a criminal offence?

A cheque bounce occurs when a cheque is dishonoured by the bank due to insufficient funds or other reasons. It becomes a criminal offence under Section 138 of the Negotiable Instruments Act, 1881, if the cheque was issued against a legally enforceable debt, presented within three months, and the drawer fails to make payment within 15 days of receiving a legal notice sent within 30 days of dishonour.

Q2. What is the procedure to file a cheque bounce case in India?

First, present the cheque to the bank within its validity. If it bounces, collect the return memo and send a legal notice to the drawer within 30 days. If payment is not made within 15 days, file a complaint before the Magistrate within the next 30 days. Submit all supporting documents, including the cheque, memo, notice copy, proof of service, and an affidavit.

Q3. What are the penalties for being convicted in a cheque bounce case in India?

If convicted under Section 138, the accused may face imprisonment for up to two years, a fine up to twice the cheque amount, or both. Courts may also order interim compensation of up to 20% during the trial. If an appeal is filed, a minimum deposit of 20% of the fine or compensation is required.

Q4. Can cheque bounce cases in India be settled outside of court?

Yes, such cases are compoundable under Section 147 of the NI Act. Settlement can happen at any stage—even during the trial or appeal—through mutual agreement, mediation, or Lok Adalat. Once settled, the court closes the case formally upon confirmation.

Q5. What legal defences are available to the accused in such cases?

The accused may claim the cheque was not for a legal debt, or was issued as a gift or security. Other defences include fraud, coercion, material alteration, or procedural lapses by the complainant. The accused can also claim prior reporting of cheque loss or theft to the bank and police.

Q6. Who can be held liable when a cheque is issued by a company?

A case can be filed against the signatory of the cheque, the company or firm itself, and any director or partner responsible for business conduct at the time. However, specific allegations about each person’s role must be clearly stated in the complaint.

Note: The above answers reflect the law and procedures as updated for 2025, including recent amendments and Supreme Court guidelines. Always consult a qualified legal professional for case-specific advice.

Why You Need an Expert Lawyer for Cheque Bounce Cases, Bengaluru

Navigating a cheque bounce case in Bengaluru requires a deep understanding of legal nuances, strict procedural compliance, and strategic litigation. Whether you are filing a complaint to recover your hard-earned money or defending against a false claim, a single misstep can be detrimental.

The team at Kapil Dixit LLP possesses the expertise and experience to guide you through every stage of the process.

We help you:

- Devise a clear plan of action.

- Ensure timely and accurate filing of notices and complaints.

- Prepare a robust case with meticulous documentation.

- Represent you effectively during trials and hearings.

Don’t let a bounced cheque disrupt your financial stability or reputation. Contact us to get expert legal help on your cheque bounce matter from the seasoned professionals at Kapil Dixit LLP.